Showing 1648–1656 of 1965 results

-

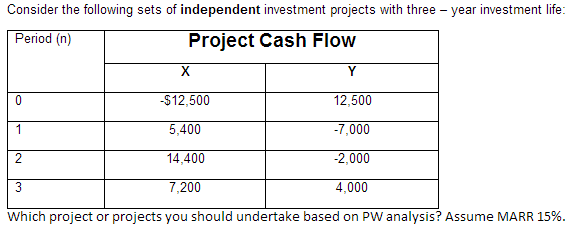

Cash flow: Which project or projects you should undertake based on PW analysis

$1.00

Text: Consider the following sets of independent investment projects with three – year investment life: Which project or projects you should undertake based on PW analysis? Assume MARR 15%.

-

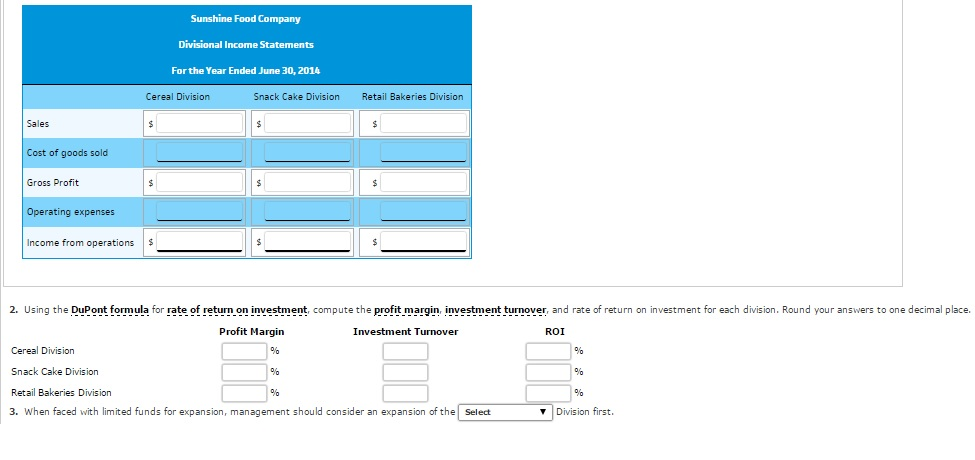

Sunshine Food Company Case: Divisional Income Statements and Rate of Return on Investment Analysis

$1.00Sunshine Food Company is a diversified food company with three operating divisions organized as investment centers. Condensed data taken from the records of the three divisions for the year ended June 30, 2014, are as follows:

Cereal

DivisionSnack Cake

DivisionRetail

Bakeries

DivisionSales $ 5,520,000 $ 5,900,000 $5,330,000 Cost of goods sold 3,370,000 3,660,000 3,140,000 Operating expenses 1,156,400 942,000 804,200 Invested assets 6,900,000 5,900,000 4,100,000 The management of Sunshine Food Company is evaluating each division as a basis for planning a future expansion of operations.

Required:

1. Prepare condensed divisional income statements for the three divisions, assuming that there were no service department charges.

-

Brodigan Corporation: Net Present Value

$1.00

Text: Brodigan Corporation has provided the following information concerning a capital budgeting project: Investment required �n equipment Net annual operating cash inflow After-tax discount rate The expected life of the project and the equipment is 3 years and the equipment has zero salvage value. The company uses straight-line depreciation on all equipment and the depreciation expense on the equipment would be dollar150,000 per year. Assume cash flows occur at the end of the year except for the initial investments. The company takes income taxes into account in its capital budgeting. The net annual operating cash inflow is the difference between the incremental sales revenue and incremental cash operating expenses. Required: Determine the net present value of the project. Show your work!

-

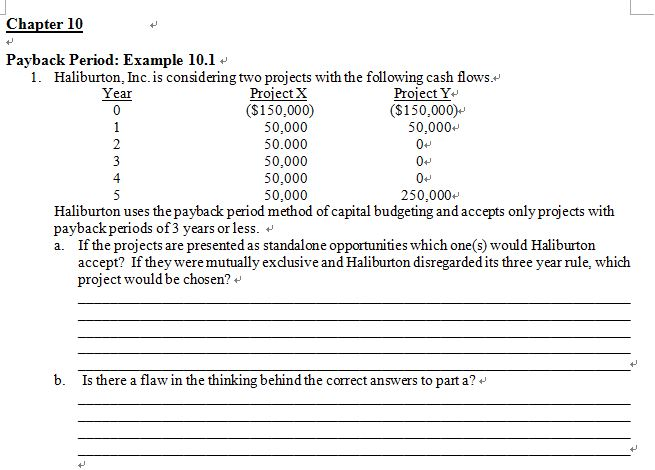

Haliburton Inc. Case

$5.00

Text: Haliburton, Inc. is considering two projects with the following cash flows. Haliburton uses the payback period method of capital budgeting and accepts only projects with payback periods of 3 years or less. a. If the projects are presented as standalone opportunities which one(s) would Haliburton accept? If they were mutually exclusive and Haliburton disregarded its three year rule, which project would be chosen? b. Is there a flaw in the thinking behind the correct answers to part a?

-

Firm’s cost of capital

$1.00The Yo-Yo Corporation tries to determine the appropriate cost for retained earnings to be used in capital budgeting analysis. The firm?s beta is t6& The rate on six-month T-buts is 169%, and the return on the S&P 500 index is 5.29%. What is the appropriate cost for retained earnings in determining the firm’s cost of capital? Round the answers to two decimal places in percentage form. (Write the percentage sign in the units box).

-

Calculate NPV for the following capital budgeting proposal

$1.00Calculate the NPV for the following capital budgeting proposal: $100,000 initial cost, to be depreciated straight-line over five years to an expected salvage value of $5,000, 35% tax rate, $45,000 additional annual revenues, $15,000 additional annual expense, $8,000 additional investment in working capital, 11% cost of capital.

-

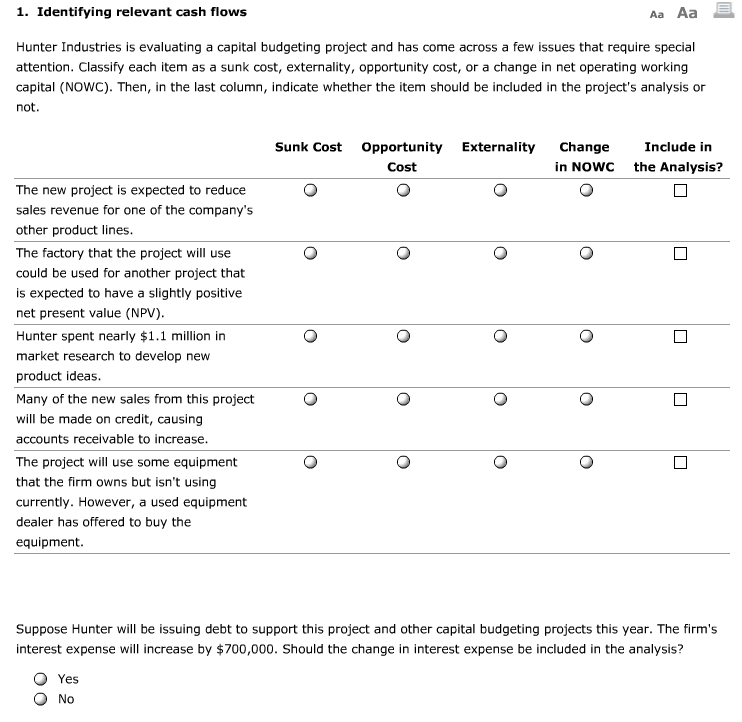

Identifying Relevant Cash Flows

$1.00

Text: Hunter Industries is evaluating a capital budgeting project and has come across a few issues that require special attention. Classify each item as a sunk cost, externality, opportunity cost, or a change in net operating working capital (NOWC). Then, in the last column, indicate whether the item should be included in the project’s analysis or Suppose Hunter will be issuing debt to support this project and other capital budgeting projects this year. The firm’s interest expense will increase by $700,000. Should the change in interest expense be included in the analysis?

-

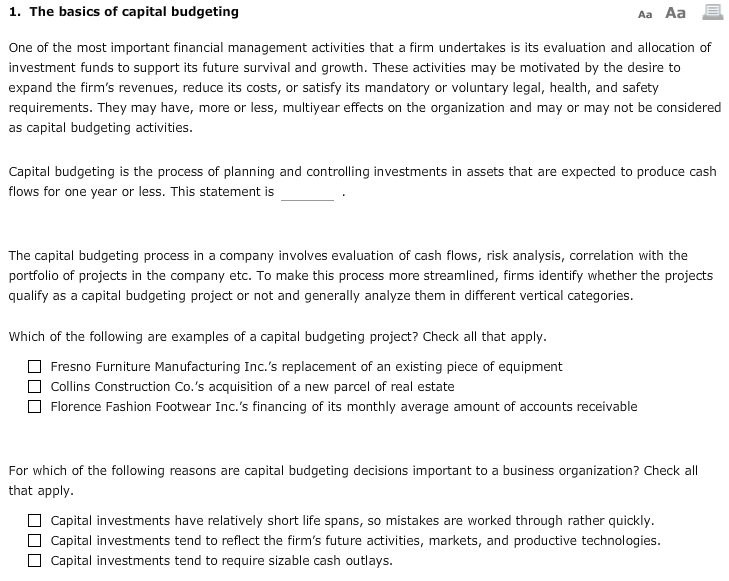

The basics of capital budgeting

$1.00

Text: One of the most important financial management activities that a firm undertakes is its evaluation and allocation of investment funds to support its future survival and growth. These activities may be motivated by the desire to expand the firm?s revenues, reduce its costs, or satisfy its mandatory or voluntary legal, health, and safety requirements. They may have, more or less, multiyear effects on the organization and may or may not be considered as capital budgeting activities. Capital budgeting is the process of planning and controlling investments in assets that are expected to produce cash flows for one year or less. This statement is . The capital budgeting process in a company involves evaluation of cash flows, risk analysis, correlation with the portfolio of projects in the company etc. To make this process more streamlined, firms identify whether the projects qualify as a capital budgeting project or not and generally analyze them in different vertical categories. Which of the following are examples of a capital budgeting project? Check all that apply. Fresno Furniture Manufacturing Inc.?s replacement of an existing piece of equipment Collins Construction Co.?s acquisition of a new parcel of real estate Florence Fashion Footwear Inc.?s financing of its monthly average amount of accounts receivable For which of the following reasons are capital budgeting decisions important to a business organization? Check all that apply. Capital investments have relatively short life spans, so mistakes are worked through rather quickly. Capital investments tend to reflect the firm?s future activities, markets, and productive technologies. Capital investments tend to require sizable cash outlays.

-

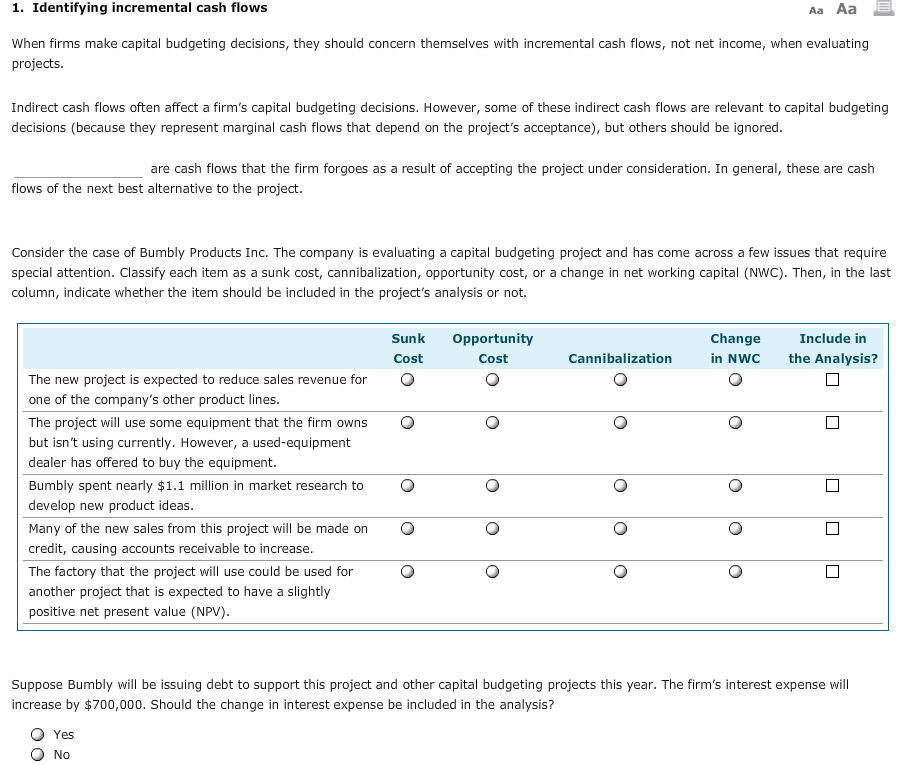

Identifying Incremental Cash Flows

$2.00When firms make capital budgeting decisions, they should concern themselves with incremental cash flows, not net income, when evaluating projects. Indirect cash flows often affect a firm?s capital budgeting decisions. However, some of these indirect cash flows are relevant to capital budgeting decisions (because they represent marginal cash flows that depend on the project?s acceptance), but others should be ignored. are cash flows that the firm forgoes as a result of accepting the project under consideration. In general, these are cash flows of the next best alternative to the project. Consider the case of Bumbly Products Inc. The company is evaluating a capital budgeting project and has come across a few issues that require special attention. Classify each item as a sunk cost, cannibalization, opportunity cost, or a change in net working capital (NWC). Then, in the last column, indicate whether the item should be included in the project?s analysis or not. Suppose Bumbly will be issuing debt to support this project and other capital budgeting projects this year. The firm?s interest expense will increase by $700,000. Should the change in interest expense be included in the analysis? Yes No